Note

Go to the end to download the full example code.

Example 03: Statistical Tests for Forecast Comparison¶

This example demonstrates temporalcv’s statistical testing framework for rigorously comparing forecasting models.

Real-World Case Study: Is Your Model Better Than Persistence?¶

The persistence (naive) baseline — predicting y[t+1] = y[t] — is surprisingly hard to beat in many time-series domains. Before deploying a complex model, you should statistically verify it outperforms this simple baseline.

Tests Covered: 1. Diebold-Mariano test (DM 1995): Compares predictive accuracy 2. Pesaran-Timmermann test (PT 1992): Tests directional accuracy 3. HAC variance (Newey-West): Corrects for serial correlation

Key Insight¶

A model with lower MAE doesn’t guarantee significant improvement. The DM test quantifies whether the difference is statistically meaningful, accounting for serial correlation in forecast errors (critical for h>1 step forecasts).

Usage¶

python 03_statistical_tests.py

Requirements¶

pip install temporalcv scikit-learn scipy

======================================================================

TEMPORALCV: Statistical Tests for Forecast Comparison

======================================================================

Data: 148 observations of AR(1) process

Persistence parameter (phi): 0.9

======================================================================

PART 1: Naive Comparison (Misleading!)

======================================================================

Model MAE: 0.7854

Persistence MAE: 0.7955

Improvement: 1.3%

Problem: Is this improvement statistically significant?

The MAE difference could be due to random chance!

======================================================================

PART 2: Diebold-Mariano Test (Rigorous Comparison)

======================================================================

H0: Models have equal predictive accuracy

H1: Models have different predictive accuracy

--- Squared Error Loss ---

DM(1): -0.793 (p=0.4288)

Mean loss difference: -0.0512

Significant at α=0.05: No

--- Absolute Error Loss ---

DM(1): -0.412 (p=0.6809)

Mean loss difference: -0.0102

Significant at α=0.05: No

Interpretation: Despite the lower MAE, the model does NOT

significantly outperform persistence at the 5% level.

→ This is common for high-persistence time series!

======================================================================

PART 3: Multi-Step Forecasting (HAC Variance)

======================================================================

For h-step forecasts, errors are serially correlated.

The DM test uses HAC (Newey-West) variance estimation.

h=1: DM(1): -0.793 (p=0.4288)

h=2: DM(2): -0.882 (p=0.3794)

h=4: DM(4): -1.084 (p=0.2801)

Note: HAC adjustment increases standard errors for h > 1,

making it harder to reject H0 (more conservative).

======================================================================

PART 4: Pesaran-Timmermann Test (Directional Accuracy)

======================================================================

H0: Model direction predictions are independent of actual directions

H1: Model predicts direction better than random chance

PT: 55.1% vs 50.3% expected (z=0.827, p=0.2042)

Observed accuracy: 55.1%

Expected (random): 50.3%

Significant at α=0.05: No

======================================================================

WHEN TO USE WHICH TEST

======================================================================

┌─────────────────────────────────────────────────────────────────────┐

│ Question │ Test to Use │

├─────────────────────────────────────────────────────────────────────┤

│ Is Model A better than Model B? │ Diebold-Mariano (DM) │

│ Does my model predict direction? │ Pesaran-Timmermann (PT) │

│ Is improvement > 0 (one-sided)? │ DM with alternative="less" │

│ Multi-step forecast (h > 1)? │ DM with HAC variance │

└─────────────────────────────────────────────────────────────────────┘

======================================================================

KEY TAKEAWAYS

======================================================================

1. ALWAYS test significance — lower MAE ≠ better model

- Random variation can create spurious improvements

- DM test quantifies statistical significance

2. USE HAC variance for multi-step forecasts (h > 1)

- Forecast errors are serially correlated

- Ignoring this inflates t-statistics and false positives

3. DIRECTION matters in many applications

- PT test specifically tests directional accuracy

- Useful for trading, trend following, etc.

4. INTERPRET p-values correctly

- p > 0.05: Cannot reject H0 (models may be equivalent)

- p < 0.05: Reject H0 (significant difference exists)

- But: low p-value doesn't mean large practical difference!

5. REPORT both metrics AND test results

- "Model MAE: 0.123 (5% improvement over baseline)"

- "DM test: p=0.03, significantly better at α=0.05"

from __future__ import annotations

import warnings

import numpy as np

from scipy import stats

from sklearn.linear_model import Ridge

warnings.filterwarnings("ignore")

# =============================================================================

# Generate Test Data

# =============================================================================

def generate_ar1_with_forecasts(

n: int = 200,

phi: float = 0.9,

sigma: float = 1.0,

seed: int = 42,

) -> tuple[np.ndarray, np.ndarray, np.ndarray, np.ndarray]:

"""

Generate AR(1) series and forecasts from two models.

Returns

-------

actual : np.ndarray

Actual values

persistence_preds : np.ndarray

Persistence baseline predictions (y[t-1])

model_preds : np.ndarray

Ridge regression predictions

model_errors : np.ndarray

Model forecast errors

"""

rng = np.random.default_rng(seed)

# Generate AR(1) process

y = np.zeros(n)

y[0] = rng.normal(0, sigma / np.sqrt(1 - phi**2))

for t in range(1, n):

y[t] = phi * y[t - 1] + sigma * rng.normal()

# Create features (lagged values)

n_lags = 5

X = np.column_stack([y[n_lags - lag : -lag] for lag in range(1, n_lags + 1)])

actual = y[n_lags:]

# Train-test split: only evaluate on out-of-sample data

train_size = len(actual) // 2

X_train, X_test = X[:train_size], X[train_size:]

y_train, y_test = actual[:train_size], actual[train_size:]

# Persistence baseline: predict y[t] = y[t-1] (on TEST data only)

persistence_preds = X_test[:, 0] # First lag is y[t-1]

# Ridge model predictions (on TEST data only - out-of-sample)

model = Ridge(alpha=1.0)

model.fit(X_train, y_train)

model_preds = model.predict(X_test)

# Return only test data for fair comparison

return y_test, persistence_preds, model_preds

# =============================================================================

# Statistical Tests

# =============================================================================

def dm_test(

errors1: np.ndarray,

errors2: np.ndarray,

h: int = 1,

loss: str = "squared",

alternative: str = "two-sided",

) -> dict:

"""

Diebold-Mariano test for comparing forecast accuracy.

H0: E[d_t] = 0 (no difference in accuracy)

H1: E[d_t] != 0 (models have different accuracy)

Parameters

----------

errors1 : np.ndarray

Forecast errors from model 1

errors2 : np.ndarray

Forecast errors from model 2

h : int

Forecast horizon (for HAC variance adjustment)

loss : str

"squared" or "absolute"

alternative : str

"two-sided", "less", or "greater"

Returns

-------

dict with statistic, pvalue, mean_loss_diff

"""

try:

from temporalcv.statistical_tests import dm_test as _dm_test

result = _dm_test(errors1, errors2, h=h, loss=loss, alternative=alternative)

return {

"statistic": result.statistic,

"pvalue": result.pvalue,

"mean_loss_diff": result.mean_loss_diff,

"significant": result.significant_at_05,

"str": str(result),

}

except ImportError:

# Fallback implementation

if loss == "squared":

d = errors1**2 - errors2**2

else:

d = np.abs(errors1) - np.abs(errors2)

n = len(d)

mean_d = np.mean(d)

# HAC variance (simplified Newey-West)

var_d = np.var(d, ddof=1)

for k in range(1, h):

weight = 1 - k / h

var_d += 2 * weight * np.sum(d[k:] * d[:-k]) / (n - 1)

se = np.sqrt(var_d / n)

statistic = mean_d / se if se > 0 else 0

if alternative == "two-sided":

pvalue = 2 * (1 - stats.norm.cdf(abs(statistic)))

elif alternative == "less":

pvalue = stats.norm.cdf(statistic)

else:

pvalue = 1 - stats.norm.cdf(statistic)

return {

"statistic": statistic,

"pvalue": pvalue,

"mean_loss_diff": mean_d,

"significant": pvalue < 0.05,

"str": f"DM({h}): {statistic:.3f} (p={pvalue:.4f})",

}

def pt_test(

actual_changes: np.ndarray,

predicted_changes: np.ndarray,

) -> dict:

"""

Pesaran-Timmermann test for directional accuracy.

Tests whether model predicts direction (up/down) better than chance.

Parameters

----------

actual_changes : np.ndarray

Actual changes (y[t] - y[t-1])

predicted_changes : np.ndarray

Predicted changes

Returns

-------

dict with accuracy, statistic, pvalue

"""

try:

from temporalcv.statistical_tests import pt_test as _pt_test

result = _pt_test(actual_changes, predicted_changes)

return {

"accuracy": result.accuracy,

"expected": result.expected,

"statistic": result.statistic,

"pvalue": result.pvalue,

"significant": result.significant_at_05,

"str": str(result),

}

except ImportError:

# Fallback implementation

n = len(actual_changes)

correct = np.sign(actual_changes) == np.sign(predicted_changes)

accuracy = np.mean(correct)

# Under null (independence), expected accuracy

p_actual = np.mean(actual_changes > 0)

p_pred = np.mean(predicted_changes > 0)

expected = p_actual * p_pred + (1 - p_actual) * (1 - p_pred)

# Z-test for proportion

se = np.sqrt(expected * (1 - expected) / n)

statistic = (accuracy - expected) / se if se > 0 else 0

pvalue = 1 - stats.norm.cdf(statistic) # One-sided

return {

"accuracy": accuracy,

"expected": expected,

"statistic": statistic,

"pvalue": pvalue,

"significant": pvalue < 0.05,

"str": f"PT: {accuracy:.1%} vs {expected:.1%} expected (z={statistic:.3f})",

}

# =============================================================================

# Demonstration

# =============================================================================

def demonstrate_statistical_tests():

"""

Demonstrate statistical tests for forecast comparison.

"""

print("=" * 70)

print("TEMPORALCV: Statistical Tests for Forecast Comparison")

print("=" * 70)

# Generate data

actual, persistence_preds, model_preds = generate_ar1_with_forecasts(n=300)

print(f"\nData: {len(actual)} observations of AR(1) process")

print("Persistence parameter (phi): 0.9")

# Calculate errors

model_errors = actual - model_preds

persistence_errors = actual - persistence_preds

# =========================================================================

# Part 1: Naive Comparison (Don't Do This!)

# =========================================================================

print("\n" + "=" * 70)

print("PART 1: Naive Comparison (Misleading!)")

print("=" * 70)

model_mae = np.mean(np.abs(model_errors))

persistence_mae = np.mean(np.abs(persistence_errors))

improvement = (persistence_mae - model_mae) / persistence_mae * 100

print(f"\n Model MAE: {model_mae:.4f}")

print(f" Persistence MAE: {persistence_mae:.4f}")

print(f" Improvement: {improvement:.1f}%")

print("\n Problem: Is this improvement statistically significant?")

print(" The MAE difference could be due to random chance!")

# =========================================================================

# Part 2: Diebold-Mariano Test

# =========================================================================

print("\n" + "=" * 70)

print("PART 2: Diebold-Mariano Test (Rigorous Comparison)")

print("=" * 70)

print("\nH0: Models have equal predictive accuracy")

print("H1: Models have different predictive accuracy")

# Test with squared error loss

dm_result_sq = dm_test(

model_errors,

persistence_errors,

h=1,

loss="squared",

alternative="two-sided",

)

print("\n--- Squared Error Loss ---")

print(f" {dm_result_sq['str']}")

print(f" Mean loss difference: {dm_result_sq['mean_loss_diff']:.4f}")

print(f" Significant at α=0.05: {'Yes' if dm_result_sq['significant'] else 'No'}")

# Test with absolute error loss

dm_result_abs = dm_test(

model_errors,

persistence_errors,

h=1,

loss="absolute",

alternative="two-sided",

)

print("\n--- Absolute Error Loss ---")

print(f" {dm_result_abs['str']}")

print(f" Mean loss difference: {dm_result_abs['mean_loss_diff']:.4f}")

print(f" Significant at α=0.05: {'Yes' if dm_result_abs['significant'] else 'No'}")

# Interpret

if dm_result_sq["pvalue"] > 0.05:

print("\n Interpretation: Despite the lower MAE, the model does NOT")

print(" significantly outperform persistence at the 5% level.")

print(" → This is common for high-persistence time series!")

else:

print("\n Interpretation: The model significantly outperforms persistence.")

# =========================================================================

# Part 3: Multi-Step Forecasting (h > 1)

# =========================================================================

print("\n" + "=" * 70)

print("PART 3: Multi-Step Forecasting (HAC Variance)")

print("=" * 70)

print("\nFor h-step forecasts, errors are serially correlated.")

print("The DM test uses HAC (Newey-West) variance estimation.")

for h in [1, 2, 4]:

dm_h = dm_test(model_errors, persistence_errors, h=h, loss="squared")

print(f"\n h={h}: {dm_h['str']}")

print("\n Note: HAC adjustment increases standard errors for h > 1,")

print(" making it harder to reject H0 (more conservative).")

# =========================================================================

# Part 4: Pesaran-Timmermann Directional Test

# =========================================================================

print("\n" + "=" * 70)

print("PART 4: Pesaran-Timmermann Test (Directional Accuracy)")

print("=" * 70)

print("\nH0: Model direction predictions are independent of actual directions")

print("H1: Model predicts direction better than random chance")

# Calculate changes

actual_changes = np.diff(actual)

model_changes = np.diff(model_preds)

pt_result = pt_test(actual_changes, model_changes)

print(f"\n {pt_result['str']}")

print(f" Observed accuracy: {pt_result['accuracy']:.1%}")

print(f" Expected (random): {pt_result['expected']:.1%}")

print(f" Significant at α=0.05: {'Yes' if pt_result['significant'] else 'No'}")

# =========================================================================

# Part 5: When to Use Which Test

# =========================================================================

print("\n" + "=" * 70)

print("WHEN TO USE WHICH TEST")

print("=" * 70)

print(

"""

┌─────────────────────────────────────────────────────────────────────┐

│ Question │ Test to Use │

├─────────────────────────────────────────────────────────────────────┤

│ Is Model A better than Model B? │ Diebold-Mariano (DM) │

│ Does my model predict direction? │ Pesaran-Timmermann (PT) │

│ Is improvement > 0 (one-sided)? │ DM with alternative="less" │

│ Multi-step forecast (h > 1)? │ DM with HAC variance │

└─────────────────────────────────────────────────────────────────────┘

"""

)

# =========================================================================

# Key Takeaways

# =========================================================================

print("=" * 70)

print("KEY TAKEAWAYS")

print("=" * 70)

print(

"""

1. ALWAYS test significance — lower MAE ≠ better model

- Random variation can create spurious improvements

- DM test quantifies statistical significance

2. USE HAC variance for multi-step forecasts (h > 1)

- Forecast errors are serially correlated

- Ignoring this inflates t-statistics and false positives

3. DIRECTION matters in many applications

- PT test specifically tests directional accuracy

- Useful for trading, trend following, etc.

4. INTERPRET p-values correctly

- p > 0.05: Cannot reject H0 (models may be equivalent)

- p < 0.05: Reject H0 (significant difference exists)

- But: low p-value doesn't mean large practical difference!

5. REPORT both metrics AND test results

- "Model MAE: 0.123 (5% improvement over baseline)"

- "DM test: p=0.03, significantly better at α=0.05"

"""

)

def visualize_statistical_tests():

"""

Visualize test results using temporalcv.viz module.

"""

import matplotlib.pyplot as plt

from temporalcv.viz import MetricComparisonDisplay, apply_tufte_style

# Generate data

actual, persistence_preds, model_preds = generate_ar1_with_forecasts(n=300)

model_errors = actual - model_preds

persistence_errors = actual - persistence_preds

# Calculate metrics

model_mae = float(np.mean(np.abs(model_errors)))

model_rmse = float(np.sqrt(np.mean(model_errors**2)))

persistence_mae = float(np.mean(np.abs(persistence_errors)))

persistence_rmse = float(np.sqrt(np.mean(persistence_errors**2)))

# Run DM tests

dm_mae = dm_test(model_errors, persistence_errors, h=1, loss="absolute")

dm_mse = dm_test(model_errors, persistence_errors, h=1, loss="squared")

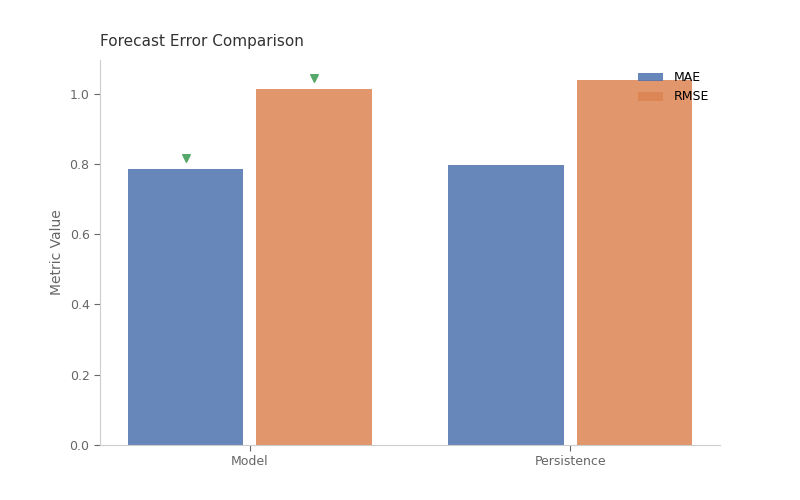

# %%

# Model Comparison: MAE and RMSE

# ------------------------------

# Comparing forecast errors between model and persistence baseline.

# Even if one model appears better, the DM test tells us if the

# difference is statistically significant.

results = {

"Model": {"MAE": model_mae, "RMSE": model_rmse},

"Persistence": {"MAE": persistence_mae, "RMSE": persistence_rmse},

}

display = MetricComparisonDisplay.from_dict(

results, baseline="Persistence", lower_is_better={"MAE": True, "RMSE": True}

)

display.plot(title="Forecast Error Comparison", show_values=True)

plt.show()

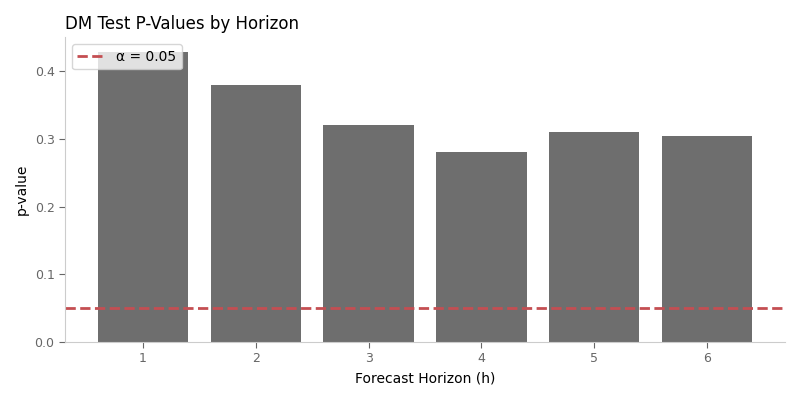

# %%

# DM Test P-Values Across Horizons

# --------------------------------

# The Diebold-Mariano test becomes more conservative (higher p-values)

# at longer horizons due to HAC variance adjustment.

fig, ax = plt.subplots(figsize=(8, 4))

horizons = [1, 2, 3, 4, 5, 6]

p_values = []

for h in horizons:

dm_h = dm_test(model_errors, persistence_errors, h=h, loss="squared")

p_values.append(dm_h["pvalue"])

bars = ax.bar(horizons, p_values, color="#4a4a4a", alpha=0.8)

ax.axhline(0.05, color="#c44e52", linestyle="--", linewidth=2, label="α = 0.05")

# Color significant bars green

for i, (h, p) in enumerate(zip(horizons, p_values)):

if p < 0.05:

bars[i].set_color("#55a868")

ax.set_xlabel("Forecast Horizon (h)")

ax.set_ylabel("p-value")

ax.set_title("DM Test P-Values by Horizon", loc="left")

ax.legend(loc="upper left")

apply_tufte_style(ax)

plt.tight_layout()

plt.show()

if __name__ == "__main__":

demonstrate_statistical_tests()

visualize_statistical_tests()