Note

Go to the end to download the full example code.

Example 04: Handling High-Persistence Time Series¶

This example demonstrates how to validate models on high-persistence data (ACF(1) > 0.9) where standard metrics can be misleading.

Real-World Case Study: Interest Rate Forecasting¶

Treasury rates, exchange rates, and many financial series have ACF(1) > 0.95. On such data: - Persistence (naive) baseline has near-zero error - Complex models struggle to beat persistence - Standard CV metrics overestimate performance

Key Metrics for High-Persistence Data: - MC-SS ratio: Model Change vs Seasonally-adjusted Series scale - MASE: Mean Absolute Scaled Error (relative to naive baseline) - DM test: Statistical comparison to persistence

Usage¶

python 04_high_persistence.py

Requirements¶

pip install temporalcv scikit-learn

from __future__ import annotations

import warnings

import matplotlib.pyplot as plt

import numpy as np

from sklearn.ensemble import GradientBoostingRegressor

from sklearn.linear_model import Ridge

from temporalcv.viz import apply_tufte_style

warnings.filterwarnings("ignore")

# =============================================================================

# Generate High-Persistence Data

# =============================================================================

def generate_high_persistence_data(

n: int = 500,

phi: float = 0.98, # Very high persistence

sigma: float = 0.05,

seed: int = 42,

) -> np.ndarray:

"""Generate high-persistence AR(1) process (like Treasury rates)."""

rng = np.random.default_rng(seed)

y = np.zeros(n)

y[0] = 3.0 + rng.normal(0, sigma / np.sqrt(1 - phi**2))

for t in range(1, n):

y[t] = phi * y[t - 1] + (1 - phi) * 3.0 + sigma * rng.normal()

return y

def create_features(series: np.ndarray, n_lags: int = 5):

"""Create lagged features."""

n = len(series)

features = []

for lag in range(1, n_lags + 1):

lagged = np.full(n, np.nan)

lagged[lag:] = series[:-lag]

features.append(lagged)

X = np.column_stack(features)

y = series.copy()

valid = ~np.isnan(X).any(axis=1)

return X[valid], y[valid]

# =============================================================================

# Metrics for High-Persistence Data

# =============================================================================

def compute_mase(actual: np.ndarray, predicted: np.ndarray, train_data: np.ndarray = None) -> float:

"""

Mean Absolute Scaled Error (Hyndman & Koehler 2006).

MASE < 1: Better than naive baseline

MASE = 1: Same as naive

MASE > 1: Worse than naive

Parameters

----------

actual : np.ndarray

Test set actual values

predicted : np.ndarray

Model predictions on test set

train_data : np.ndarray, optional

Training data for computing naive baseline scale.

If None, uses actual (test data) for backward compatibility,

but this is NOT recommended per MASE definition.

"""

mae = np.mean(np.abs(actual - predicted))

# Naive baseline MAE should be computed from TRAINING data per MASE definition

if train_data is not None:

naive_mae = np.mean(np.abs(np.diff(train_data)))

else:

# Fallback: compute from test data (not recommended)

naive_mae = np.mean(np.abs(np.diff(actual)))

return mae / naive_mae if naive_mae > 0 else np.inf

def compute_mc_ss_ratio(actual: np.ndarray, predicted: np.ndarray) -> float:

"""

Model Change vs Series Scale ratio.

For high-persistence data, changes are tiny relative to series level.

This metric normalizes by the series scale.

"""

mae = np.mean(np.abs(actual - predicted))

series_scale = np.std(actual)

return mae / series_scale if series_scale > 0 else np.inf

def compute_directional_accuracy(actual: np.ndarray, predicted: np.ndarray) -> float:

"""Proportion of correct direction predictions."""

actual_changes = np.diff(actual)

pred_changes = np.diff(predicted)

return np.mean(np.sign(actual_changes) == np.sign(pred_changes))

# =============================================================================

# Demonstration

# =============================================================================

def demonstrate_high_persistence():

"""Demonstrate handling of high-persistence data."""

print("=" * 70)

print("TEMPORALCV: Handling High-Persistence Time Series")

print("=" * 70)

# Generate data

series = generate_high_persistence_data()

acf1 = np.corrcoef(series[1:], series[:-1])[0, 1]

print("\nData characteristics:")

print(f" Length: {len(series)}")

print(f" Mean: {np.mean(series):.2f}")

print(f" Std: {np.std(series):.4f}")

print(f" ACF(1): {acf1:.4f} (HIGH persistence)")

# Create features

X, y = create_features(series)

train_size = int(0.7 * len(y))

X_train, X_test = X[:train_size], X[train_size:]

y_train, y_test = y[:train_size], y[train_size:]

print(f"\n Train: {len(X_train)} samples")

print(f" Test: {len(X_test)} samples")

# =========================================================================

# Part 1: The Persistence Baseline Problem

# =========================================================================

print("\n" + "=" * 70)

print("PART 1: The Persistence Baseline Problem")

print("=" * 70)

# Persistence predictions

persistence_preds = X_test[:, 0] # y[t-1]

persistence_mae = np.mean(np.abs(y_test - persistence_preds))

print(f"\n Persistence baseline MAE: {persistence_mae:.6f}")

print(" Persistence MASE: 1.000 (by definition)")

print(" This is an EXTREMELY tough baseline to beat!")

# =========================================================================

# Part 2: Model Comparison

# =========================================================================

print("\n" + "=" * 70)

print("PART 2: Model Comparison")

print("=" * 70)

models = {

"Ridge (simple)": Ridge(alpha=1.0),

"GBM (complex)": GradientBoostingRegressor(n_estimators=50, max_depth=2, random_state=42),

}

results = []

for name, model in models.items():

model.fit(X_train, y_train)

preds = model.predict(X_test)

mae = np.mean(np.abs(y_test - preds))

# Pass y_train for MASE denominator per Hyndman & Koehler 2006

mase = compute_mase(y_test, preds, train_data=y_train)

mc_ss = compute_mc_ss_ratio(y_test, preds)

dir_acc = compute_directional_accuracy(y_test, preds)

results.append(

{

"name": name,

"mae": mae,

"mase": mase,

"mc_ss": mc_ss,

"dir_acc": dir_acc,

}

)

print(f"\n {name}:")

print(f" MAE: {mae:.6f} (vs persistence: {persistence_mae:.6f})")

print(f" MASE: {mase:.3f} {'✓ <1' if mase < 1 else '✗ ≥1'}")

print(f" MC/SS: {mc_ss:.3f}")

print(f" Direction accuracy: {dir_acc:.1%}")

# =========================================================================

# Part 3: Why Standard Metrics Mislead

# =========================================================================

print("\n" + "=" * 70)

print("PART 3: Why Standard Metrics Mislead")

print("=" * 70)

print(

"""

For high-persistence data (ACF(1) > 0.95):

┌─────────────────────────────────────────────────────────────────────┐

│ Metric │ Problem │ Better Alternative │

├─────────────────────────────────────────────────────────────────────┤

│ MAE/RMSE │ Near-zero for persistence │ MASE (scaled) │

│ R² │ Near 1.0 even for naive models │ Out-of-sample R² │

│ % Error │ Meaningless when y ≈ constant │ Relative to baseline │

└─────────────────────────────────────────────────────────────────────┘

"""

)

# =========================================================================

# Part 4: Validation Strategy

# =========================================================================

print("=" * 70)

print("PART 4: Recommended Validation Strategy")

print("=" * 70)

print(

"""

1. ALWAYS compare to persistence baseline

- If MASE ≥ 1, your model doesn't beat naive

- Use DM test to verify statistical significance

2. LOOK at directional accuracy

- Even 55% accuracy can be valuable for trading

- Use PT test for statistical significance

3. USE walk-forward CV with sufficient gap

- Prevents leakage from feature engineering

- Reflects realistic deployment scenario

4. MONITOR regime changes

- High-persistence ≠ stationary

- Sliding window may outperform expanding

5. BE SKEPTICAL of impressive metrics

- MAE of 0.001 is meaningless if persistence achieves 0.0005

- Always report relative metrics (MASE, % improvement)

"""

)

# =========================================================================

# Part 5: Summary Table

# =========================================================================

print("=" * 70)

print("SUMMARY TABLE")

print("=" * 70)

print(f"\n{'Model':<20} {'MAE':<12} {'MASE':<8} {'Direction':<10} {'Verdict':<15}")

print("-" * 65)

print(f"{'Persistence':<20} {persistence_mae:<12.6f} {'1.000':<8} {'-':<10} {'Baseline':<15}")

for r in results:

verdict = "✓ Better" if r["mase"] < 1 else "✗ No better"

print(

f"{r['name']:<20} {r['mae']:<12.6f} {r['mase']:<8.3f} {r['dir_acc']:<10.1%} {verdict:<15}"

)

if __name__ == "__main__":

demonstrate_high_persistence()

======================================================================

TEMPORALCV: Handling High-Persistence Time Series

======================================================================

Data characteristics:

Length: 500

Mean: 2.98

Std: 0.1695

ACF(1): 0.9593 (HIGH persistence)

Train: 346 samples

Test: 149 samples

======================================================================

PART 1: The Persistence Baseline Problem

======================================================================

Persistence baseline MAE: 0.039061

Persistence MASE: 1.000 (by definition)

This is an EXTREMELY tough baseline to beat!

======================================================================

PART 2: Model Comparison

======================================================================

Ridge (simple):

MAE: 0.046039 (vs persistence: 0.039061)

MASE: 1.222 ✗ ≥1

MC/SS: 0.268

Direction accuracy: 50.7%

GBM (complex):

MAE: 0.043450 (vs persistence: 0.039061)

MASE: 1.154 ✗ ≥1

MC/SS: 0.253

Direction accuracy: 50.0%

======================================================================

PART 3: Why Standard Metrics Mislead

======================================================================

For high-persistence data (ACF(1) > 0.95):

┌─────────────────────────────────────────────────────────────────────┐

│ Metric │ Problem │ Better Alternative │

├─────────────────────────────────────────────────────────────────────┤

│ MAE/RMSE │ Near-zero for persistence │ MASE (scaled) │

│ R² │ Near 1.0 even for naive models │ Out-of-sample R² │

│ % Error │ Meaningless when y ≈ constant │ Relative to baseline │

└─────────────────────────────────────────────────────────────────────┘

======================================================================

PART 4: Recommended Validation Strategy

======================================================================

1. ALWAYS compare to persistence baseline

- If MASE ≥ 1, your model doesn't beat naive

- Use DM test to verify statistical significance

2. LOOK at directional accuracy

- Even 55% accuracy can be valuable for trading

- Use PT test for statistical significance

3. USE walk-forward CV with sufficient gap

- Prevents leakage from feature engineering

- Reflects realistic deployment scenario

4. MONITOR regime changes

- High-persistence ≠ stationary

- Sliding window may outperform expanding

5. BE SKEPTICAL of impressive metrics

- MAE of 0.001 is meaningless if persistence achieves 0.0005

- Always report relative metrics (MASE, % improvement)

======================================================================

SUMMARY TABLE

======================================================================

Model MAE MASE Direction Verdict

-----------------------------------------------------------------

Persistence 0.039061 1.000 - Baseline

Ridge (simple) 0.046039 1.222 50.7% ✗ No better

GBM (complex) 0.043450 1.154 50.0% ✗ No better

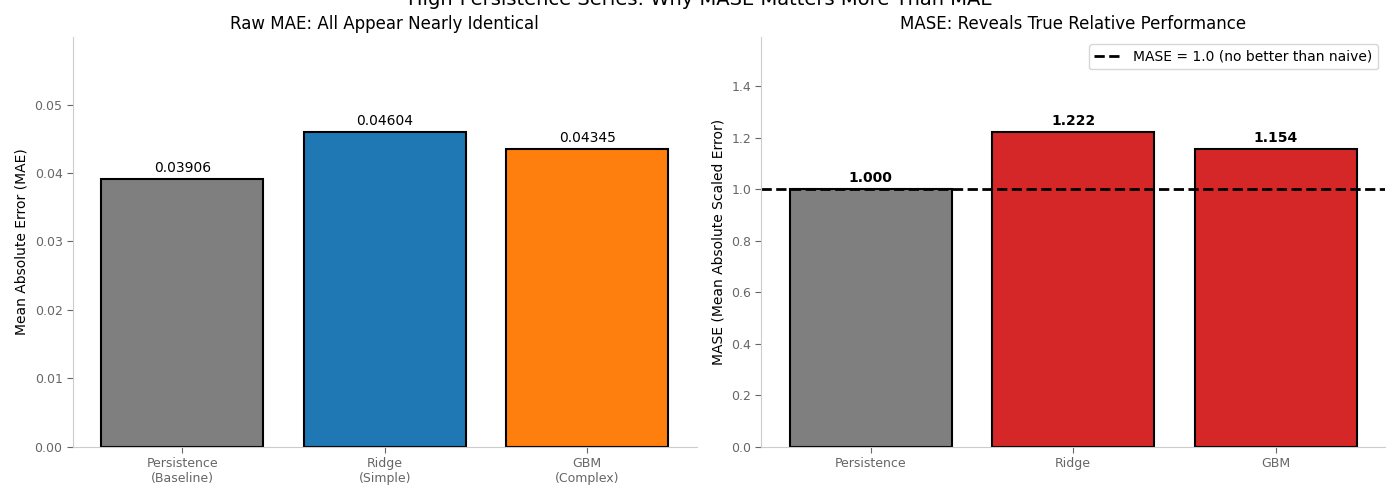

Visualization: High-Persistence Metrics Comparison¶

This plot shows why MASE matters for high-persistence series and compares model performance relative to the persistence baseline.

# Generate data and fit models for visualization

series = generate_high_persistence_data()

X, y = create_features(series)

train_size = int(0.7 * len(y))

X_train, X_test = X[:train_size], X[train_size:]

y_train, y_test = y[:train_size], y[train_size:]

# Fit models

ridge = Ridge(alpha=1.0)

ridge.fit(X_train, y_train)

ridge_preds = ridge.predict(X_test)

gbm = GradientBoostingRegressor(n_estimators=50, max_depth=2, random_state=42)

gbm.fit(X_train, y_train)

gbm_preds = gbm.predict(X_test)

# Persistence baseline

persistence_preds = X_test[:, 0]

# Compute metrics

persistence_mae = np.mean(np.abs(y_test - persistence_preds))

ridge_mae = np.mean(np.abs(y_test - ridge_preds))

gbm_mae = np.mean(np.abs(y_test - gbm_preds))

ridge_mase = compute_mase(y_test, ridge_preds, train_data=y_train)

gbm_mase = compute_mase(y_test, gbm_preds, train_data=y_train)

# Create visualization

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Left: MAE comparison (shows why raw MAE is misleading)

ax1 = axes[0]

models = ["Persistence\n(Baseline)", "Ridge\n(Simple)", "GBM\n(Complex)"]

maes = [persistence_mae, ridge_mae, gbm_mae]

colors = ["#7f7f7f", "#1f77b4", "#ff7f0e"]

bars = ax1.bar(models, maes, color=colors, edgecolor="black", linewidth=1.5)

ax1.set_ylabel("Mean Absolute Error (MAE)")

ax1.set_title("Raw MAE: All Appear Nearly Identical")

ax1.set_ylim(0, max(maes) * 1.3)

for bar, mae in zip(bars, maes):

ax1.annotate(

f"{mae:.5f}",

xy=(bar.get_x() + bar.get_width() / 2, bar.get_height()),

xytext=(0, 3),

textcoords="offset points",

ha="center",

va="bottom",

fontsize=10,

)

# Right: MASE comparison (reveals true relative performance)

ax2 = axes[1]

models_mase = ["Persistence", "Ridge", "GBM"]

mases = [1.0, ridge_mase, gbm_mase]

colors_mase = [

"#7f7f7f",

"#2ca02c" if ridge_mase < 1 else "#d62728",

"#2ca02c" if gbm_mase < 1 else "#d62728",

]

bars2 = ax2.bar(models_mase, mases, color=colors_mase, edgecolor="black", linewidth=1.5)

ax2.axhline(

1.0, color="black", linestyle="--", linewidth=2, label="MASE = 1.0 (no better than naive)"

)

ax2.set_ylabel("MASE (Mean Absolute Scaled Error)")

ax2.set_title("MASE: Reveals True Relative Performance")

ax2.set_ylim(0, max(mases) * 1.3)

ax2.legend(loc="upper right")

for bar, mase in zip(bars2, mases):

label = f"{mase:.3f}"

if mase < 1:

label += " ✓"

ax2.annotate(

label,

xy=(bar.get_x() + bar.get_width() / 2, bar.get_height()),

xytext=(0, 3),

textcoords="offset points",

ha="center",

va="bottom",

fontsize=10,

fontweight="bold",

)

# Apply Tufte styling

for ax in axes:

apply_tufte_style(ax)

plt.tight_layout()

plt.suptitle("High-Persistence Series: Why MASE Matters More Than MAE", y=1.02, fontsize=14)

plt.show()