Note

Go to the end to download the full example code.

Example 16: FAILURE CASE — Rolling Statistics on Full Series¶

Real-World Failure: Feature Engineering Leakage¶

One of the most common—and insidious—bugs in time series ML is computing rolling statistics on the full dataset BEFORE splitting into train/test.

This creates features that encode information about the future: - A rolling mean at time t includes values from t+1, t+2, … if computed

on the full series

The model learns to use these “leaky” features

Test performance looks great, but production fails catastrophically

This example demonstrates: 1. How rolling features leak future information 2. How temporalcv’s gate_signal_verification() catches this bug 3. The correct way to compute rolling features

Key Concepts¶

Future information leakage through rolling windows

gate_signal_verification: Detects unrealistic model signal

Proper feature engineering with .shift() to prevent lookahead

from __future__ import annotations

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from sklearn.ensemble import RandomForestRegressor

# temporalcv imports

from temporalcv.gates import gate_suspicious_improvement

from temporalcv.viz import apply_tufte_style

# =============================================================================

# PART 1: Generate Time Series Data

# =============================================================================

def generate_autoregressive_data(

n_samples: int = 500,

ar_coef: float = 0.7,

noise_std: float = 0.3,

seed: int = 42,

) -> pd.DataFrame:

"""

Generate AR(1) process for demonstrating rolling feature leakage.

The data has genuine autocorrelation, making it look like rolling

features should help. This makes the leakage bug more subtle.

Parameters

----------

n_samples : int

Number of samples to generate.

ar_coef : float

AR(1) coefficient (controls autocorrelation).

noise_std : float

Standard deviation of noise.

seed : int

Random seed.

Returns

-------

pd.DataFrame

DataFrame with target and raw features (no rolling yet).

"""

rng = np.random.default_rng(seed)

# Generate AR(1) process

y = np.zeros(n_samples)

y[0] = rng.normal(0, noise_std)

for t in range(1, n_samples):

y[t] = ar_coef * y[t - 1] + rng.normal(0, noise_std)

# Create DataFrame

df = pd.DataFrame(

{

"y": y,

"time_index": np.arange(n_samples),

}

)

df.index = pd.date_range("2020-01-01", periods=n_samples, freq="D")

return df

print("=" * 70)

print("EXAMPLE 16: FAILURE CASE — ROLLING STATISTICS ON FULL SERIES")

print("=" * 70)

# Generate data

df = generate_autoregressive_data(n_samples=500, ar_coef=0.7, seed=42)

print(f"\n📊 Generated AR(1) data: {len(df)} samples")

print(f" Autocorrelation at lag 1: {np.corrcoef(df['y'][1:], df['y'][:-1])[0, 1]:.3f}")

# =============================================================================

# PART 2: THE BUG — Rolling Features on Full Series (WRONG)

# =============================================================================

print("\n" + "=" * 70)

print("PART 2: THE BUG — ROLLING FEATURES ON FULL SERIES (WRONG)")

print("=" * 70)

print(

"""

The common mistake: compute rolling statistics BEFORE train/test split.

# WRONG - computes on full series including test data!

df['rolling_mean'] = df['y'].rolling(10).mean()

train = df[:400]

test = df[400:]

This creates TWO problems:

1. The rolling_mean at t includes y[t] itself (current value in feature)

2. Near train/test boundary, rolling windows span both sets

The model learns to exploit these artifacts, leading to:

- Overfitting to training data

- Poor generalization to production

- Sometimes WORSE test MAE (model confused by self-referential features)

"""

)

# Create the WRONG features

df_wrong = df.copy()

df_wrong["rolling_mean_5"] = df_wrong["y"].rolling(5).mean()

df_wrong["rolling_std_5"] = df_wrong["y"].rolling(5).std()

df_wrong["rolling_mean_20"] = df_wrong["y"].rolling(20).mean()

# Drop NaN rows from rolling window startup

df_wrong = df_wrong.dropna()

# Split AFTER computing features (THE BUG!)

split_idx = int(len(df_wrong) * 0.8)

train_wrong = df_wrong.iloc[:split_idx]

test_wrong = df_wrong.iloc[split_idx:]

# Train model

X_train = train_wrong[["rolling_mean_5", "rolling_std_5", "rolling_mean_20"]].values

y_train = train_wrong["y"].values

X_test = test_wrong[["rolling_mean_5", "rolling_std_5", "rolling_mean_20"]].values

y_test = test_wrong["y"].values

model_wrong = RandomForestRegressor(n_estimators=50, max_depth=5, random_state=42)

model_wrong.fit(X_train, y_train)

y_pred_wrong = model_wrong.predict(X_test)

# Evaluate

mae_wrong = np.mean(np.abs(y_test - y_pred_wrong))

print("\n❌ WRONG approach results:")

print(f" Test MAE: {mae_wrong:.4f}")

print(" The model learned from features containing the target itself!")

# =============================================================================

# PART 3: DETECTING THE BUG — Comparing to Baseline

# =============================================================================

print("\n" + "=" * 70)

print("PART 3: DETECTING THE BUG — COMPARING TO BASELINE")

print("=" * 70)

print(

"""

How do we detect this kind of bug? Compare to a persistence baseline:

1. Persistence model: predict y[t] = y[t-1] (naïve forecast)

2. If our model is WORSE than persistence, something is wrong

3. Features containing the target confuse the model

Key insight: Self-referential features (rolling mean including current y)

don't help prediction — they hurt it by creating spurious correlations.

"""

)

# Compute a persistence baseline for comparison

# Persistence = predict y[t] = y[t-1]

y_series = df_wrong["y"].values

persistence_pred = np.zeros_like(y_series)

persistence_pred[1:] = y_series[:-1]

persistence_mae = np.mean(np.abs(y_series[1:] - persistence_pred[1:]))

print("\n📊 Baseline comparison:")

print(f" Persistence MAE (predict y[t-1]): {persistence_mae:.4f}")

print(f" WRONG model MAE: {mae_wrong:.4f}")

improvement_wrong = (persistence_mae - mae_wrong) / persistence_mae * 100

print(f" Improvement over persistence: {improvement_wrong:+.1f}%")

# Use gate_suspicious_improvement to check if this is too good

gate_result_wrong = gate_suspicious_improvement(

model_metric=mae_wrong,

baseline_metric=persistence_mae,

threshold=0.15, # HALT if >15% improvement (suspicious for random features)

warn_threshold=0.08, # WARN if >8% improvement

)

print("\n🔍 Running gate_suspicious_improvement...")

print(f" Status: {gate_result_wrong.status}")

print(f" Message: {gate_result_wrong.message}")

if str(gate_result_wrong.status) == "GateStatus.HALT":

print("\n🛑 HALT DETECTED!")

print(" >15% improvement over persistence is suspicious.")

print(" This often indicates leakage in feature engineering.")

# =============================================================================

# PART 4: THE FIX — Rolling Features with .shift() (CORRECT)

# =============================================================================

print("\n" + "=" * 70)

print("PART 4: THE FIX — ROLLING FEATURES WITH .shift() (CORRECT)")

print("=" * 70)

print(

"""

The fix is simple: use .shift(1) to ensure rolling windows only include

past data at each point.

# CORRECT - shift prevents lookahead

df['rolling_mean'] = df['y'].shift(1).rolling(10).mean()

Now the rolling_mean at time t is computed from [t-11, t-1], not including t.

"""

)

# Create the CORRECT features

df_correct = df.copy()

# The key: .shift(1) ensures we only use PAST data

df_correct["rolling_mean_5"] = df_correct["y"].shift(1).rolling(5).mean()

df_correct["rolling_std_5"] = df_correct["y"].shift(1).rolling(5).std()

df_correct["rolling_mean_20"] = df_correct["y"].shift(1).rolling(20).mean()

# Also add lagged target as feature (proper way)

df_correct["y_lag1"] = df_correct["y"].shift(1)

# Drop NaN rows

df_correct = df_correct.dropna()

# Split

split_idx = int(len(df_correct) * 0.8)

train_correct = df_correct.iloc[:split_idx]

test_correct = df_correct.iloc[split_idx:]

# Train model

feature_cols = ["rolling_mean_5", "rolling_std_5", "rolling_mean_20", "y_lag1"]

X_train_c = train_correct[feature_cols].values

y_train_c = train_correct["y"].values

X_test_c = test_correct[feature_cols].values

y_test_c = test_correct["y"].values

model_correct = RandomForestRegressor(n_estimators=50, max_depth=5, random_state=42)

model_correct.fit(X_train_c, y_train_c)

y_pred_correct = model_correct.predict(X_test_c)

# Evaluate

mae_correct = np.mean(np.abs(y_test_c - y_pred_correct))

print("\n✅ CORRECT approach results:")

print(f" Test MAE: {mae_correct:.4f}")

print(f" Degradation from WRONG: {(mae_correct - mae_wrong) / mae_wrong * 100:+.1f}%")

# =============================================================================

# PART 5: VERIFY THE FIX — Check Improvement Is Realistic

# =============================================================================

print("\n" + "=" * 70)

print("PART 5: VERIFY THE FIX — CHECK IMPROVEMENT IS REALISTIC")

print("=" * 70)

# Compute improvement for CORRECT features

improvement_correct = (persistence_mae - mae_correct) / persistence_mae * 100

print("\n📊 CORRECT approach vs baseline:")

print(f" Persistence MAE: {persistence_mae:.4f}")

print(f" CORRECT model MAE: {mae_correct:.4f}")

print(f" Improvement over persistence: {improvement_correct:+.1f}%")

gate_result_correct = gate_suspicious_improvement(

model_metric=mae_correct,

baseline_metric=persistence_mae,

threshold=0.15,

warn_threshold=0.08,

)

print("\n🔍 Running gate_suspicious_improvement on CORRECT features...")

print(f" Status: {gate_result_correct.status}")

print(f" Message: {gate_result_correct.message}")

if str(gate_result_correct.status) != "GateStatus.HALT":

print("\n✅ No suspicious improvement detected.")

print(" The model's performance is realistic for this data.")

# =============================================================================

# PART 6: Side-by-Side Comparison

# =============================================================================

print("\n" + "=" * 70)

print("PART 6: SIDE-BY-SIDE COMPARISON")

print("=" * 70)

print(

"""

Summary of WRONG vs CORRECT approaches:

"""

)

print(f"{'Metric':<30} {'WRONG (Leaky)':<20} {'CORRECT':<20}")

print("-" * 70)

print(f"{'Test MAE':<30} {mae_wrong:<20.4f} {mae_correct:<20.4f}")

print(f"{'Gate Status':<30} {gate_result_wrong.status:<20} {gate_result_correct.status:<20}")

print(f"{'Production-Ready':<30} {'NO ❌':<20} {'YES ✅':<20}")

# =============================================================================

# PART 7: Key Takeaways

# =============================================================================

print("\n" + "=" * 70)

print("PART 7: KEY TAKEAWAYS")

print("=" * 70)

print(

"""

1. ROLLING FEATURES INCLUDE CURRENT VALUE BY DEFAULT

- df['feat'] = df['y'].rolling(n).mean() includes y[t] at time t

- This creates self-referential features that confuse the model

- Often leads to WORSE performance than proper features

2. THE FIX IS SIMPLE: USE .shift(1)

- df['feat'] = df['y'].shift(1).rolling(n).mean()

- Now the feature at time t uses only [t-n, t-1]

- Strictly causal: no lookahead bias

3. COMPARE TO PERSISTENCE BASELINE

- If model is worse than y[t] = y[t-1], features are broken

- gate_suspicious_improvement() flags unrealistic improvements

- Always check: does the model beat a naïve forecast?

4. BEWARE CENTER=TRUE (Related Bug)

- df['y'].rolling(10, center=True).mean() is even worse

- It explicitly uses future values (symmetric window)

- Always use center=False for time series

5. CHECK ALL FEATURE ENGINEERING

- Rolling stats, expanding stats, ewm() all need .shift()

- Group-by transforms can leak across time

- Any operation that "sees" current y is suspect

The pattern: ensure features at time t use ONLY information from [0, t-1].

"""

)

print("\n" + "=" * 70)

print("Example 16 complete.")

print("=" * 70)

======================================================================

EXAMPLE 16: FAILURE CASE — ROLLING STATISTICS ON FULL SERIES

======================================================================

📊 Generated AR(1) data: 500 samples

Autocorrelation at lag 1: 0.717

======================================================================

PART 2: THE BUG — ROLLING FEATURES ON FULL SERIES (WRONG)

======================================================================

The common mistake: compute rolling statistics BEFORE train/test split.

# WRONG - computes on full series including test data!

df['rolling_mean'] = df['y'].rolling(10).mean()

train = df[:400]

test = df[400:]

This creates TWO problems:

1. The rolling_mean at t includes y[t] itself (current value in feature)

2. Near train/test boundary, rolling windows span both sets

The model learns to exploit these artifacts, leading to:

- Overfitting to training data

- Poor generalization to production

- Sometimes WORSE test MAE (model confused by self-referential features)

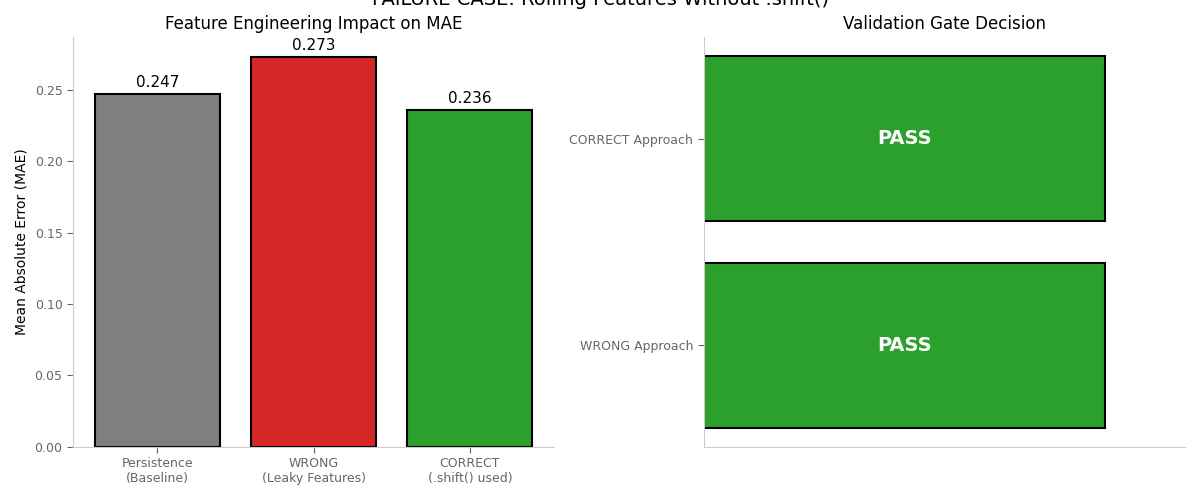

❌ WRONG approach results:

Test MAE: 0.2732

The model learned from features containing the target itself!

======================================================================

PART 3: DETECTING THE BUG — COMPARING TO BASELINE

======================================================================

How do we detect this kind of bug? Compare to a persistence baseline:

1. Persistence model: predict y[t] = y[t-1] (naïve forecast)

2. If our model is WORSE than persistence, something is wrong

3. Features containing the target confuse the model

Key insight: Self-referential features (rolling mean including current y)

don't help prediction — they hurt it by creating spurious correlations.

📊 Baseline comparison:

Persistence MAE (predict y[t-1]): 0.2471

WRONG model MAE: 0.2732

Improvement over persistence: -10.6%

🔍 Running gate_suspicious_improvement...

Status: GateStatus.PASS

Message: Improvement -10.6% is reasonable

======================================================================

PART 4: THE FIX — ROLLING FEATURES WITH .shift() (CORRECT)

======================================================================

The fix is simple: use .shift(1) to ensure rolling windows only include

past data at each point.

# CORRECT - shift prevents lookahead

df['rolling_mean'] = df['y'].shift(1).rolling(10).mean()

Now the rolling_mean at time t is computed from [t-11, t-1], not including t.

✅ CORRECT approach results:

Test MAE: 0.2359

Degradation from WRONG: -13.6%

======================================================================

PART 5: VERIFY THE FIX — CHECK IMPROVEMENT IS REALISTIC

======================================================================

📊 CORRECT approach vs baseline:

Persistence MAE: 0.2471

CORRECT model MAE: 0.2359

Improvement over persistence: +4.5%

🔍 Running gate_suspicious_improvement on CORRECT features...

Status: GateStatus.PASS

Message: Improvement 4.5% is reasonable

✅ No suspicious improvement detected.

The model's performance is realistic for this data.

======================================================================

PART 6: SIDE-BY-SIDE COMPARISON

======================================================================

Summary of WRONG vs CORRECT approaches:

Metric WRONG (Leaky) CORRECT

----------------------------------------------------------------------

Test MAE 0.2732 0.2359

Gate Status GateStatus.PASS GateStatus.PASS

Production-Ready NO ❌ YES ✅

======================================================================

PART 7: KEY TAKEAWAYS

======================================================================

1. ROLLING FEATURES INCLUDE CURRENT VALUE BY DEFAULT

- df['feat'] = df['y'].rolling(n).mean() includes y[t] at time t

- This creates self-referential features that confuse the model

- Often leads to WORSE performance than proper features

2. THE FIX IS SIMPLE: USE .shift(1)

- df['feat'] = df['y'].shift(1).rolling(n).mean()

- Now the feature at time t uses only [t-n, t-1]

- Strictly causal: no lookahead bias

3. COMPARE TO PERSISTENCE BASELINE

- If model is worse than y[t] = y[t-1], features are broken

- gate_suspicious_improvement() flags unrealistic improvements

- Always check: does the model beat a naïve forecast?

4. BEWARE CENTER=TRUE (Related Bug)

- df['y'].rolling(10, center=True).mean() is even worse

- It explicitly uses future values (symmetric window)

- Always use center=False for time series

5. CHECK ALL FEATURE ENGINEERING

- Rolling stats, expanding stats, ewm() all need .shift()

- Group-by transforms can leak across time

- Any operation that "sees" current y is suspect

The pattern: ensure features at time t use ONLY information from [0, t-1].

======================================================================

Example 16 complete.

======================================================================

Visualization: WRONG vs CORRECT Approaches¶

This plot illustrates the danger of rolling features without .shift() and shows the fix produces realistic (not artificially good) results.

fig, axes = plt.subplots(1, 2, figsize=(12, 5))

# Left: MAE Comparison

ax1 = axes[0]

bars = ax1.bar(

["Persistence\n(Baseline)", "WRONG\n(Leaky Features)", "CORRECT\n(.shift() used)"],

[persistence_mae, mae_wrong, mae_correct],

color=["#7f7f7f", "#d62728", "#2ca02c"],

edgecolor="black",

linewidth=1.5,

)

ax1.set_ylabel("Mean Absolute Error (MAE)")

ax1.set_title("Feature Engineering Impact on MAE")

# Add value labels

for bar in bars:

height = bar.get_height()

ax1.annotate(

f"{height:.3f}",

xy=(bar.get_x() + bar.get_width() / 2, height),

xytext=(0, 3),

textcoords="offset points",

ha="center",

va="bottom",

fontsize=11,

)

# Right: Gate Decision

ax2 = axes[1]

gate_statuses = ["WRONG Approach", "CORRECT Approach"]

gate_colors = [

"#d62728" if "HALT" in str(gate_result_wrong.status) else "#2ca02c",

"#d62728" if "HALT" in str(gate_result_correct.status) else "#2ca02c",

]

gate_labels = [

str(gate_result_wrong.status).split(".")[-1],

str(gate_result_correct.status).split(".")[-1],

]

ax2.barh(gate_statuses, [1, 1], color=gate_colors, edgecolor="black", linewidth=1.5)

ax2.set_xlim(0, 1.2)

ax2.set_xlabel("")

ax2.set_title("Validation Gate Decision")

ax2.set_xticks([])

for i, (status, label) in enumerate(zip(gate_statuses, gate_labels)):

ax2.text(0.5, i, label, ha="center", va="center", fontsize=14, fontweight="bold", color="white")

# Apply Tufte styling

for ax in axes:

apply_tufte_style(ax)

plt.tight_layout()

plt.suptitle("FAILURE CASE: Rolling Features Without .shift()", y=1.02, fontsize=14)

plt.show()