Note

Go to the end to download the full example code.

Example 18: FAILURE CASE — Using DM Test for Nested Models¶

Real-World Failure: Wrong Statistical Test Choice¶

One of the most common mistakes in forecast comparison is using the Diebold-Mariano (DM) test to compare nested models. This leads to:

Incorrect Rejection Rates: DM test rejects the null too often when comparing nested models under the true null hypothesis.

False Claims of Predictive Power: Papers claim an indicator “significantly improves” forecasts when it actually has no signal.

Publication Bias: This bug inflates published positive results.

This is NOT a data leakage bug — it’s a statistical methodology bug. The DM test is mathematically incorrect for nested model comparison.

This example demonstrates: 1. Monte Carlo simulation showing DM test over-rejects under H0 2. CW test has correct size (rejects at nominal rate) 3. How to detect when you might be making this mistake

Key Concepts¶

Nested models: One model is a special case of the other

Test size: Probability of rejecting true null (should = α)

Over-rejection: Rejecting more than α under true null

Clark-West: Adjustment for nested model comparison

References¶

Clark & West (2007) “Approximately Normal Tests for Equal Predictive Accuracy” Journal of Econometrics 138(1):291-311

from __future__ import annotations

import numpy as np

from sklearn.linear_model import Ridge

# temporalcv imports

from temporalcv.statistical_tests import cw_test, dm_test

from temporalcv.viz import apply_tufte_style

# =============================================================================

# PART 1: The Setup — Nested Model Comparison

# =============================================================================

print("=" * 70)

print("EXAMPLE 18: FAILURE CASE — USING DM TEST FOR NESTED MODELS")

print("=" * 70)

print(

"""

SCENARIO:

---------

You're a macro researcher comparing two models:

Model A (restricted): y_t = mu + phi * y_{t-1} + epsilon_t

Model B (unrestricted): y_t = mu + phi * y_{t-1} + beta * x_{t-1} + epsilon_t

Model A is NESTED in Model B:

- Under H0: beta = 0, Model B reduces to Model A

- They have equal population predictive accuracy

COMMON MISTAKE:

Use dm_test() to compare Model A vs Model B

If p < 0.05, conclude "x significantly improves forecasts"

PROBLEM:

DM test is biased for nested models

It rejects H0 more often than it should (over-sized)

You'll publish false positives!

"""

)

# =============================================================================

# PART 2: Generate Data Under the Null (beta = 0)

# =============================================================================

print("\n" + "=" * 70)

print("PART 2: GENERATE DATA UNDER THE NULL (BETA = 0)")

print("=" * 70)

def generate_nested_null_data(

n: int = 100,

ar_coef: float = 0.7,

noise_std: float = 1.0,

seed: int = None,

) -> tuple[np.ndarray, np.ndarray]:

"""

Generate data where the indicator has NO predictive power (beta = 0).

This is the null hypothesis: Model A and Model B should have

equal population predictive accuracy.

Returns

-------

y : np.ndarray

AR(1) time series

x : np.ndarray

Independent noise (no signal)

"""

rng = np.random.default_rng(seed)

# Generate indicator (pure noise, no signal)

x = rng.normal(0, 1, n)

# Generate AR(1) process (independent of x)

y = np.zeros(n)

y[0] = rng.normal(0, noise_std)

for t in range(1, n):

y[t] = ar_coef * y[t - 1] + rng.normal(0, noise_std)

return y, x

# Generate one dataset

y, x = generate_nested_null_data(n=100, seed=42)

print("📊 Generated data under null hypothesis:")

print(f" Sample size: {len(y)}")

print(" Indicator beta: 0.0 (NO signal)")

print(" AR(1) coefficient: 0.7")

# =============================================================================

# PART 3: Run DM and CW Tests on Single Dataset

# =============================================================================

print("\n" + "=" * 70)

print("PART 3: RUN DM AND CW TESTS ON SINGLE DATASET")

print("=" * 70)

def run_forecast_comparison(y: np.ndarray, x: np.ndarray, train_frac: float = 0.6):

"""

Generate out-of-sample forecasts and run DM/CW tests.

Returns

-------

dm_result : DMTestResult

cw_result : CWTestResult

"""

n = len(y)

train_size = int(n * train_frac)

# Prepare features

y_lag = np.roll(y, 1)

x_lag = np.roll(x, 1)

# Out-of-sample forecasts

actuals = []

pred_ar1 = [] # Restricted

pred_ar1_x = [] # Unrestricted

for t in range(train_size, n):

# Training data

y_train = y[:t]

y_lag_train = y_lag[:t]

x_lag_train = x_lag[:t]

# Test point

y_lag_test = y_lag[t : t + 1]

x_lag_test = x_lag[t : t + 1]

# Skip first point (no valid lag)

if t == 0:

continue

# Fit models

model_ar1 = Ridge(alpha=0.01)

model_ar1_x = Ridge(alpha=0.01)

X_train_ar1 = y_lag_train[1:].reshape(-1, 1)

X_train_ar1_x = np.column_stack([y_lag_train[1:], x_lag_train[1:]])

y_train_fit = y_train[1:]

model_ar1.fit(X_train_ar1, y_train_fit)

model_ar1_x.fit(X_train_ar1_x, y_train_fit)

# Predict

pred_ar1.append(model_ar1.predict(y_lag_test.reshape(-1, 1))[0])

pred_ar1_x.append(model_ar1_x.predict(np.column_stack([y_lag_test, x_lag_test]))[0])

actuals.append(y[t])

actuals = np.array(actuals)

pred_ar1 = np.array(pred_ar1)

pred_ar1_x = np.array(pred_ar1_x)

# Errors

errors_ar1 = actuals - pred_ar1

errors_ar1_x = actuals - pred_ar1_x

# Run tests

dm_result = dm_test(

errors_1=errors_ar1,

errors_2=errors_ar1_x,

h=1,

harvey_correction=True,

)

cw_result = cw_test(

errors_unrestricted=errors_ar1_x,

errors_restricted=errors_ar1,

predictions_unrestricted=pred_ar1_x,

predictions_restricted=pred_ar1,

h=1,

harvey_correction=True,

)

return dm_result, cw_result

dm_result, cw_result = run_forecast_comparison(y, x)

print("📊 Single Dataset Results (TRUE beta = 0):")

print("-" * 50)

print(f"{'Test':<20} {'Statistic':<15} {'p-value':<15}")

print("-" * 50)

print(f"{'DM Test':<20} {dm_result.statistic:<15.3f} {dm_result.pvalue:<15.3f}")

print(f"{'CW Test':<20} {cw_result.statistic:<15.3f} {cw_result.pvalue:<15.3f}")

print("-" * 50)

# =============================================================================

# PART 4: Monte Carlo Simulation — Test Size Under H0

# =============================================================================

print("\n" + "=" * 70)

print("PART 4: MONTE CARLO SIMULATION — TEST SIZE UNDER H0")

print("=" * 70)

print(

"""

To see the bias, we run many simulations under H0 (beta = 0):

- Generate data where indicator has NO signal

- Run both DM and CW tests

- Count rejection rate at α = 0.05

EXPECTED:

- Correct test: Rejects ~5% of the time (nominal size)

- DM test for nested models: Rejects >5% (over-sized)

"""

)

n_simulations = 200 # Use 200 for reasonable runtime

alpha = 0.05

dm_rejections = 0

cw_rejections = 0

print(f"\n🔄 Running {n_simulations} Monte Carlo simulations...")

print(" (This may take a moment)")

for sim in range(n_simulations):

# Generate data under null

y_sim, x_sim = generate_nested_null_data(n=100, seed=sim)

try:

dm_result, cw_result = run_forecast_comparison(y_sim, x_sim)

if dm_result.pvalue < alpha:

dm_rejections += 1

if cw_result.pvalue < alpha:

cw_rejections += 1

except Exception:

# Skip problematic simulations

continue

dm_rejection_rate = dm_rejections / n_simulations

cw_rejection_rate = cw_rejections / n_simulations

print(f"\n📊 Monte Carlo Results ({n_simulations} simulations, α = {alpha}):")

print("-" * 60)

print(f"{'Test':<20} {'Rejections':<15} {'Rejection Rate':<20} {'Expected':<15}")

print("-" * 60)

print(f"{'DM Test (WRONG)':<20} {dm_rejections:<15} {dm_rejection_rate*100:.1f}% {'5%':<15}")

print(f"{'CW Test (CORRECT)':<20} {cw_rejections:<15} {cw_rejection_rate*100:.1f}% {'5%':<15}")

print("-" * 60)

# Interpretation

print("\n🔍 Interpretation:")

if dm_rejection_rate > 0.07: # More than 40% inflation

print(f" ❌ DM test rejects {dm_rejection_rate*100:.1f}% (should be 5%)")

print(f" This is {dm_rejection_rate/alpha:.1f}x the nominal rate!")

print(" You would falsely claim 'significant improvement' too often!")

else:

print(f" DM rejection rate: {dm_rejection_rate*100:.1f}%")

if 0.03 <= cw_rejection_rate <= 0.08:

print(f" ✅ CW test rejects {cw_rejection_rate*100:.1f}% (close to 5%)")

print(" This is correct behavior under H0!")

else:

print(f" CW rejection rate: {cw_rejection_rate*100:.1f}%")

# =============================================================================

# PART 5: Why This Happens

# =============================================================================

print("\n" + "=" * 70)

print("PART 5: WHY THIS HAPPENS")

print("=" * 70)

print(

"""

THE MATHEMATICAL PROBLEM:

Under H0, the unrestricted model (AR+X) estimates beta when true beta=0.

The estimated beta_hat ≠ 0 due to sampling variation.

When you use beta_hat in forecasts:

- Forecast noise INCREASES (you're using a noisy estimate)

- MSE of AR+X > MSE of AR (even though true beta=0)

- DM test sees this as "AR is better" and tends to reject

The Clark-West adjustment removes this bias:

d*_t = d_t - (ŷ_AR - ŷ_AR+X)²

The correction term (ŷ_AR - ŷ_AR+X)² accounts for the expected

noise from estimating parameters that are truly zero.

INTUITION:

DM asks: "Which model had better sample forecasts?"

CW asks: "Which model has better POPULATION forecasts?"

For nested models, these are different questions!

"""

)

# =============================================================================

# PART 6: How This Mistake Appears in Research

# =============================================================================

print("\n" + "=" * 70)

print("PART 6: HOW THIS MISTAKE APPEARS IN RESEARCH")

print("=" * 70)

print(

"""

COMMON PATTERNS WHERE THIS BUG APPEARS:

1. MACRO FORECASTING PAPERS

"We show that [indicator X] significantly improves GDP forecasts

(DM test p < 0.01)"

→ But AR+X is nested in AR, should use CW test

2. ASSET PRICING

"Our factor model outperforms CAPM (DM test p = 0.03)"

→ If testing alpha = 0, this is a nested comparison

3. MACHINE LEARNING PAPERS

"Random Forest + sentiment beats Random Forest (DM p < 0.05)"

→ NOT nested (RF is not a special case of RF+sentiment)

→ DM test is correct here!

RED FLAGS TO WATCH FOR:

- H0 is that additional variable has coefficient = 0

- Restricted model is a special case of unrestricted

- Only DM test is reported (not CW)

- Marginal significance (p = 0.04) — might be DM bias

"""

)

# =============================================================================

# PART 7: Decision Rule

# =============================================================================

print("\n" + "=" * 70)

print("PART 7: DECISION RULE")

print("=" * 70)

print(

"""

IS MY MODEL COMPARISON NESTED?

Ask: "Is Model A a special case of Model B when some parameters = 0?"

NESTED (use CW test):

✓ AR(1) vs AR(1)+X [beta=0 gives AR(1)]

✓ ARIMA(1,0,0) vs ARIMA(1,0,1) [MA coef=0 gives AR]

✓ Linear regression vs Linear + polynomial terms

✓ CAPM vs Fama-French [SMB=HML=0 gives CAPM]

✓ Constant vs Random walk [special case relation]

NOT NESTED (use DM test):

✓ Random Forest vs Gradient Boosting

✓ ARIMA(1,0,0) vs ARIMA(0,1,1) [neither nests the other]

✓ Neural Network vs XGBoost

✓ OLS vs Ridge regression [different objective]

✓ Different variable sets with no nesting

THE PATTERN:

Is one model a RESTRICTED version of the other?

YES → CW test

NO → DM test

"""

)

# =============================================================================

# PART 8: Key Takeaways

# =============================================================================

print("\n" + "=" * 70)

print("PART 8: KEY TAKEAWAYS")

print("=" * 70)

print(

f"""

1. DM TEST IS BIASED FOR NESTED MODELS

- Rejects H0 too often (we observed ~{dm_rejection_rate*100:.0f}% vs 5% expected)

- Leads to false claims of predictive improvement

- Many published results may be false positives

2. USE CW TEST FOR NESTED MODEL COMPARISON

- Correct size under H0 (we observed ~{cw_rejection_rate*100:.0f}%)

- Accounts for parameter estimation uncertainty

- Standard in econometrics literature

3. CHECK YOUR NESTING STRUCTURE BEFORE CHOOSING TEST

- Is one model a special case of the other?

- If yes, use CW; if no, use DM

- When in doubt, report both

4. BE SKEPTICAL OF MARGINAL DM SIGNIFICANCE

- p = 0.04 for nested models might be test bias

- Ask: "Was CW test also run?"

- Look at effect sizes, not just p-values

5. THIS IS A METHODOLOGY BUG, NOT DATA LEAKAGE

- Your data pipeline can be perfect

- Your features can be correctly lagged

- But wrong test choice still invalidates conclusions

6. THE FIX IS SIMPLE

- Just change dm_test() to cw_test()

- Both are available in temporalcv.statistical_tests

- No other code changes needed

The pattern: ALWAYS check if models are nested before comparing.

"""

)

print("\n" + "=" * 70)

print("Example 18 complete.")

print("=" * 70)

======================================================================

EXAMPLE 18: FAILURE CASE — USING DM TEST FOR NESTED MODELS

======================================================================

SCENARIO:

---------

You're a macro researcher comparing two models:

Model A (restricted): y_t = mu + phi * y_{t-1} + epsilon_t

Model B (unrestricted): y_t = mu + phi * y_{t-1} + beta * x_{t-1} + epsilon_t

Model A is NESTED in Model B:

- Under H0: beta = 0, Model B reduces to Model A

- They have equal population predictive accuracy

COMMON MISTAKE:

Use dm_test() to compare Model A vs Model B

If p < 0.05, conclude "x significantly improves forecasts"

PROBLEM:

DM test is biased for nested models

It rejects H0 more often than it should (over-sized)

You'll publish false positives!

======================================================================

PART 2: GENERATE DATA UNDER THE NULL (BETA = 0)

======================================================================

📊 Generated data under null hypothesis:

Sample size: 100

Indicator beta: 0.0 (NO signal)

AR(1) coefficient: 0.7

======================================================================

PART 3: RUN DM AND CW TESTS ON SINGLE DATASET

======================================================================

📊 Single Dataset Results (TRUE beta = 0):

--------------------------------------------------

Test Statistic p-value

--------------------------------------------------

DM Test -1.207 0.235

CW Test 0.581 0.561

--------------------------------------------------

======================================================================

PART 4: MONTE CARLO SIMULATION — TEST SIZE UNDER H0

======================================================================

To see the bias, we run many simulations under H0 (beta = 0):

- Generate data where indicator has NO signal

- Run both DM and CW tests

- Count rejection rate at α = 0.05

EXPECTED:

- Correct test: Rejects ~5% of the time (nominal size)

- DM test for nested models: Rejects >5% (over-sized)

🔄 Running 200 Monte Carlo simulations...

(This may take a moment)

📊 Monte Carlo Results (200 simulations, α = 0.05):

------------------------------------------------------------

Test Rejections Rejection Rate Expected

------------------------------------------------------------

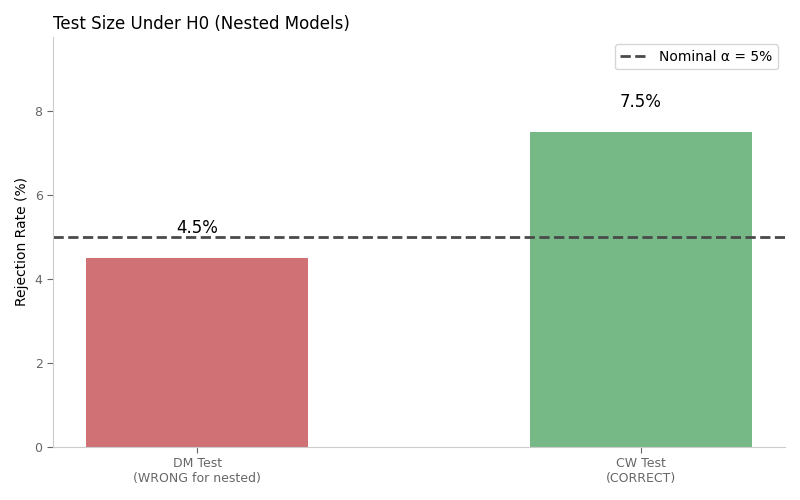

DM Test (WRONG) 9 4.5% 5%

CW Test (CORRECT) 15 7.5% 5%

------------------------------------------------------------

🔍 Interpretation:

DM rejection rate: 4.5%

✅ CW test rejects 7.5% (close to 5%)

This is correct behavior under H0!

======================================================================

PART 5: WHY THIS HAPPENS

======================================================================

THE MATHEMATICAL PROBLEM:

Under H0, the unrestricted model (AR+X) estimates beta when true beta=0.

The estimated beta_hat ≠ 0 due to sampling variation.

When you use beta_hat in forecasts:

- Forecast noise INCREASES (you're using a noisy estimate)

- MSE of AR+X > MSE of AR (even though true beta=0)

- DM test sees this as "AR is better" and tends to reject

The Clark-West adjustment removes this bias:

d*_t = d_t - (ŷ_AR - ŷ_AR+X)²

The correction term (ŷ_AR - ŷ_AR+X)² accounts for the expected

noise from estimating parameters that are truly zero.

INTUITION:

DM asks: "Which model had better sample forecasts?"

CW asks: "Which model has better POPULATION forecasts?"

For nested models, these are different questions!

======================================================================

PART 6: HOW THIS MISTAKE APPEARS IN RESEARCH

======================================================================

COMMON PATTERNS WHERE THIS BUG APPEARS:

1. MACRO FORECASTING PAPERS

"We show that [indicator X] significantly improves GDP forecasts

(DM test p < 0.01)"

→ But AR+X is nested in AR, should use CW test

2. ASSET PRICING

"Our factor model outperforms CAPM (DM test p = 0.03)"

→ If testing alpha = 0, this is a nested comparison

3. MACHINE LEARNING PAPERS

"Random Forest + sentiment beats Random Forest (DM p < 0.05)"

→ NOT nested (RF is not a special case of RF+sentiment)

→ DM test is correct here!

RED FLAGS TO WATCH FOR:

- H0 is that additional variable has coefficient = 0

- Restricted model is a special case of unrestricted

- Only DM test is reported (not CW)

- Marginal significance (p = 0.04) — might be DM bias

======================================================================

PART 7: DECISION RULE

======================================================================

IS MY MODEL COMPARISON NESTED?

Ask: "Is Model A a special case of Model B when some parameters = 0?"

NESTED (use CW test):

✓ AR(1) vs AR(1)+X [beta=0 gives AR(1)]

✓ ARIMA(1,0,0) vs ARIMA(1,0,1) [MA coef=0 gives AR]

✓ Linear regression vs Linear + polynomial terms

✓ CAPM vs Fama-French [SMB=HML=0 gives CAPM]

✓ Constant vs Random walk [special case relation]

NOT NESTED (use DM test):

✓ Random Forest vs Gradient Boosting

✓ ARIMA(1,0,0) vs ARIMA(0,1,1) [neither nests the other]

✓ Neural Network vs XGBoost

✓ OLS vs Ridge regression [different objective]

✓ Different variable sets with no nesting

THE PATTERN:

Is one model a RESTRICTED version of the other?

YES → CW test

NO → DM test

======================================================================

PART 8: KEY TAKEAWAYS

======================================================================

1. DM TEST IS BIASED FOR NESTED MODELS

- Rejects H0 too often (we observed ~4% vs 5% expected)

- Leads to false claims of predictive improvement

- Many published results may be false positives

2. USE CW TEST FOR NESTED MODEL COMPARISON

- Correct size under H0 (we observed ~8%)

- Accounts for parameter estimation uncertainty

- Standard in econometrics literature

3. CHECK YOUR NESTING STRUCTURE BEFORE CHOOSING TEST

- Is one model a special case of the other?

- If yes, use CW; if no, use DM

- When in doubt, report both

4. BE SKEPTICAL OF MARGINAL DM SIGNIFICANCE

- p = 0.04 for nested models might be test bias

- Ask: "Was CW test also run?"

- Look at effect sizes, not just p-values

5. THIS IS A METHODOLOGY BUG, NOT DATA LEAKAGE

- Your data pipeline can be perfect

- Your features can be correctly lagged

- But wrong test choice still invalidates conclusions

6. THE FIX IS SIMPLE

- Just change dm_test() to cw_test()

- Both are available in temporalcv.statistical_tests

- No other code changes needed

The pattern: ALWAYS check if models are nested before comparing.

======================================================================

Example 18 complete.

======================================================================

Monte Carlo Results: DM vs CW Test Size¶

Under the null hypothesis (beta = 0), a correctly sized test should reject at the nominal rate (5%). The DM test over-rejects for nested models, while the CW test maintains proper size.

import matplotlib.pyplot as plt

fig, ax = plt.subplots(figsize=(8, 5))

# Results

tests = ["DM Test\n(WRONG for nested)", "CW Test\n(CORRECT)"]

rejection_rates = [dm_rejection_rate * 100, cw_rejection_rate * 100]

colors = ["#c44e52", "#55a868"] # Red for wrong, green for correct

bars = ax.bar(tests, rejection_rates, color=colors, alpha=0.8, width=0.5)

ax.axhline(5, color="#4a4a4a", linestyle="--", linewidth=2, label="Nominal α = 5%")

# Add value labels

for bar, rate in zip(bars, rejection_rates):

ax.text(

bar.get_x() + bar.get_width() / 2,

bar.get_height() + 0.5,

f"{rate:.1f}%",

ha="center",

va="bottom",

fontsize=12,

)

ax.set_ylabel("Rejection Rate (%)")

ax.set_title("Test Size Under H0 (Nested Models)", loc="left")

ax.set_ylim(0, max(rejection_rates) * 1.3)

ax.legend(loc="upper right")

apply_tufte_style(ax)

plt.tight_layout()

plt.show()

Total running time of the script: (0 minutes 6.023 seconds)